Help & support

Products and services

Protect yourself from scams

Learn about the different types of scams, how to spot a scam, and ways to keep yourself safe.

Protect your bestie with Pet Insurance

Get two months' free insurance and claim up to 90% on eligible vet bills. Issued by PetSure (Australia) Pty Ltd. T&Cs apply. Consider PDS and TMD before buying.

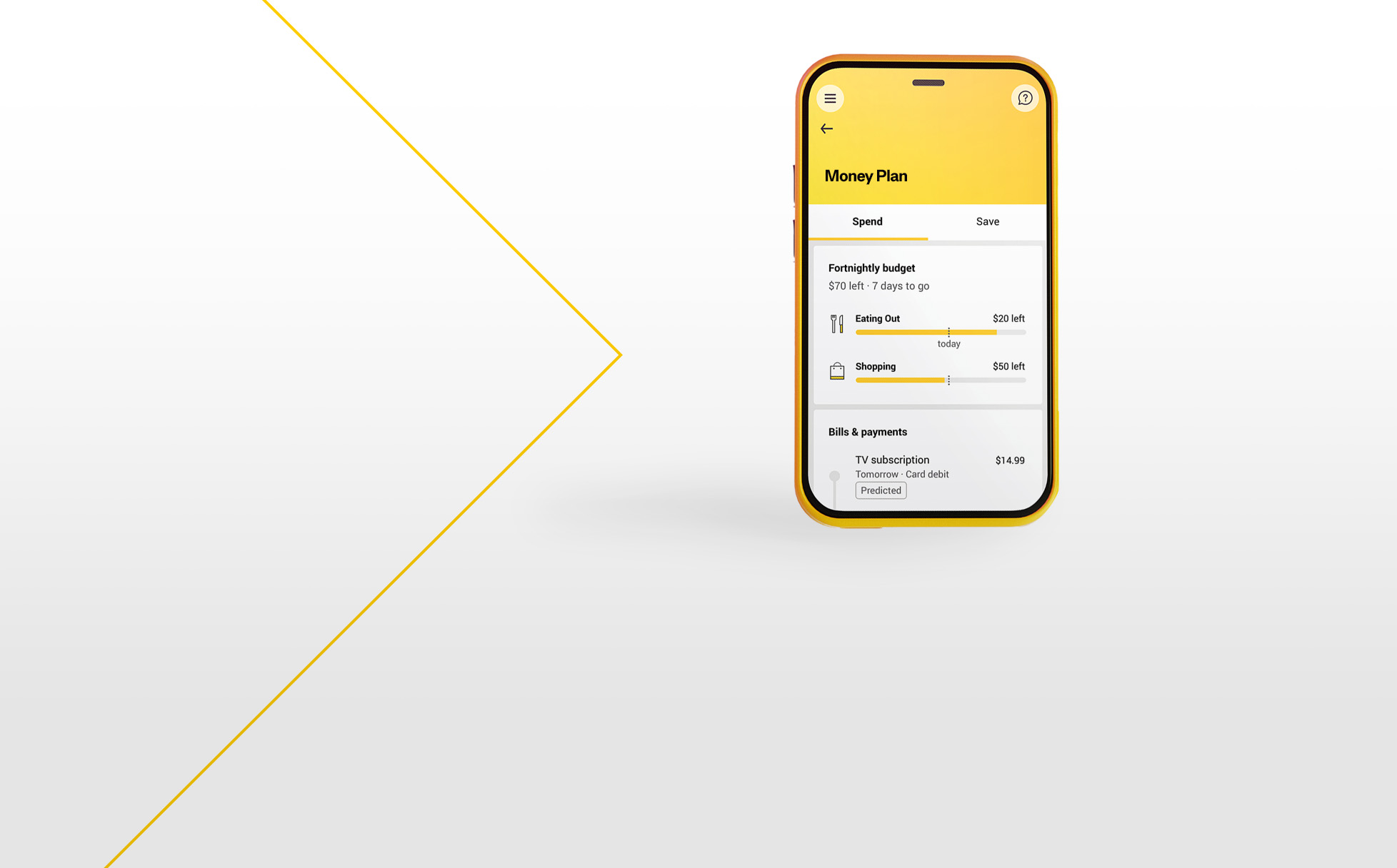

Securely grow your savings

Earn 4.75% p.a. with a 12-month Term Deposit on balances from $5,000 to $1,999,999. Limited time only. Eligibility criteria and T&Cs apply.