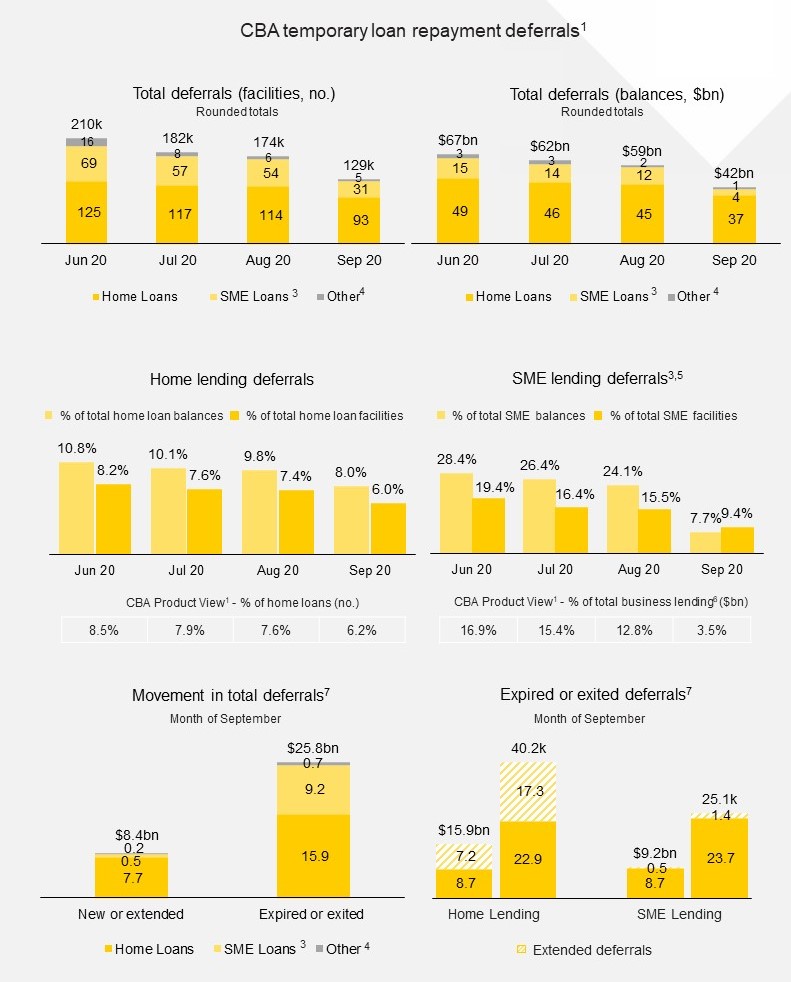

Latest figures for September show an encouraging trend in the number of our home loan and SME lending customers who are able to return to making repayments on their loans. As a result, the total number of loan repayment deferrals now sits at 129,000, down from 174,000 in August and 210,000 in June. Total loan balances on these deferrals now stand at $42bn, down from $59bn in August and $67bn in June. Further significant reductions are expected as initial temporary repayment deferrals continue to expire through October.

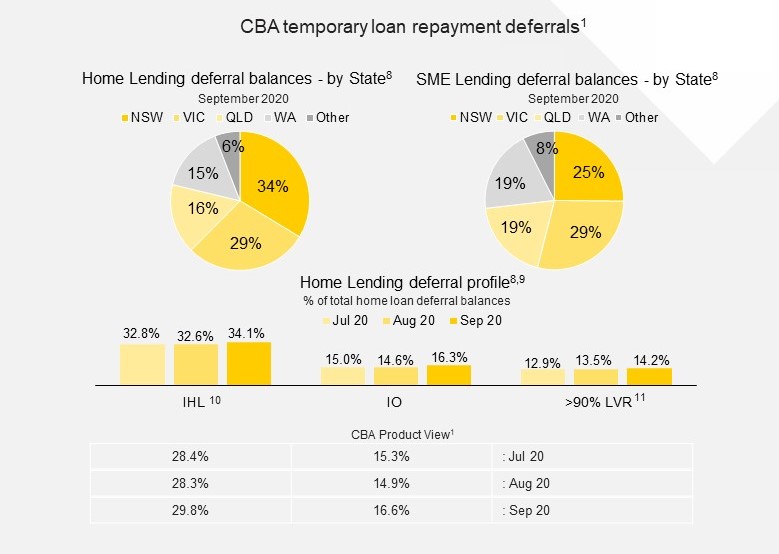

While these trends are encouraging, we are conscious that many of our customers still require our ongoing support, particularly in regions most affected by COVID-19, such as Victoria, which is reflected in requests for deferral extensions. We will continue to offer support and assistance to our customers as the economy recovers.”

Footnotes

- COVID-19 temporary loan repayment deferral data as reported to APRA, based on the domestic lending book with segmented reporting for housing and SME lending (defined as lending to clients with total loan facilities up to $10m). Data is categorised and reported based on predominant loan purpose, which differs to a product-based categorisation (Product View) used in the preparation of the Group’s financial results. Together with other definitional and classification differences noted against specific metrics and as outlined in footnotes below, this results in some differences in reported deferral numbers relative to APRA reporting. For reference, key metrics under both APRA reporting definitions and the CBA Product View are shown where relevant.

- Deferral extensions subject to eligibility criteria. Extension periods of up to 4 months for a maximum total deferral period of 10 months from the start of the repayment deferral, or until 31 March 2021, whichever comes first.

- Includes asset finance leases. SME Government Guarantee loans are excluded from SME loan deferral totals from July 2020.

- ‘Other’ includes home loans with a predominant personal purpose and non-SME business loans (>$10m).

- CBA’s relatively high proportion of SME loans in deferral reflects the Bank’s pro-active auto-deferral of SME loans where customers had borrowing limits up to $5m. Movement in September reflects the roll-off of auto-deferred business loans with the remaining deferrals largely comprised of asset finance leases.

- Total business lending deferral balances as a percentage of total business lending balances (including exposures >$10m, ex Institutional Lending).

- New or extended loan deferrals include deferrals where an extension has been granted in the month. Expired or exited deferrals include deferrals exited in the month or where an extension has been granted in the month.

- Excludes loan deferrals that do not receive capital concession.

- Home loan exiting deferrals have been over-represented in the Owner-Occupied, Principal and Interest and <90% LVR segments, resulting in increases in the proportion of remaining deferrals in Investment, Interest Only and >90% LVR segments.

- Per APRA’s EFS data collection, ‘Investment housing loan’ refers to a loan to a household for the purpose of housing where the funds are used for a residential property that is not owner-occupied and is not the principal place of residence.

- Current LVR as per APS112 definition. This differs from Dynamic LVR numbers reported in the Group’s financial results, which reflect collateral values updated monthly. August increase reflects limited exits from deferrals from the higher LVR segment.

Important Information

The material in this announcement is general background information about the Group and its activities current as at the date of the announcement, 12 October 2020. It is information given in summary form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. Investors should consult with their own legal, tax, business and/or financial advisors in connection with any investment decision.