It’s March 2020 and the world has suddenly become a much more dangerous place, health-wise

COVID-19 is quietly but swiftly spreading across the globe. Australia is not immune nor a safe haven.

It’s March 2020 and the world has suddenly become a much more dangerous place, health-wise

COVID-19 is quietly but swiftly spreading across the globe. Australia is not immune nor a safe haven.

After the alarm bells started ringing in late January with the first recognised domestic cases of coronavirus infection, the following five weeks would underscore the health, social and economic risks caused by a worldwide pandemic not seen since the Spanish Flu outbreak 100 years before.

Very quickly and ominously the “P” word dominated everyday conversation. And as more and more restrictions on our daily lives were introduced, there would be no getting away from the topic and, for that matter, COVID-19 itself unless we literally went into isolation. Which we subsequently did in a nationwide effort to try to contain and supress the virus.

The signs of what were to come were highlighted by the Federal Government’s activation on 27 February of the country’s Health Sector Emergency Response Plan as the virus began to spread from the original source of its outbreak.

Less than four days later, with the first Australian to die from the effects of COVID-19 and the first cases of community transmission reported, in NSW, the wider and potentially devastating impacts on the country’s economy began to sink in.

The Government had already started work on its first financial stimulus package, subsequently described by Prime Minister Scott Morrison and Treasurer Josh Frydenberg as measures designed to “protect Australians' health, secure jobs and set the economy to bounce back” from the growing crisis when it was unveiled on 12 March.

But before that, there had already been intensive and detailed discussions behind the scenes with Australia’s major banks about how they could provide effective help and support for millions of people – their customers – who were facing a wave of lost jobs, lost income and, in the worst case scenario, the loss of their homes.

For Matt Comyn, CEO of the Commonwealth Bank of Australia and the chair of the Australian Banking Association, which represents the overwhelming number of the country’s lenders, this was the moment when the industry had to stand up.

Without the banks’ getting behind their customers, there would be no telling how many Australians would be facing an extremely bleak future and that had to be avoided or at least alleviated as much as (and as quickly as) possible.

“Australia has a strong and stable financial system and economy, and we recognise the important role we play to support our customers, our people, our suppliers and the economy,” Commonwealth Bank Chief Executive Officer, Matt Comyn, said in a statement at the time.

The first steps – announced by Commonwealth Bank on 10 March – were designed to do two things: build confidence that CBA and the broader financial system was strong, able to withstand the economic shocks; and provide re-assurance to customers that the bank would stand behind them.

That announcement included measures to support home loan customers, those needing to use the group’s 900-strong branch network, people needing to switch to digital banking and, for those running small and medium size businesses, reductions to business loan rates, faster lending decisions and loan deferrals where needed.

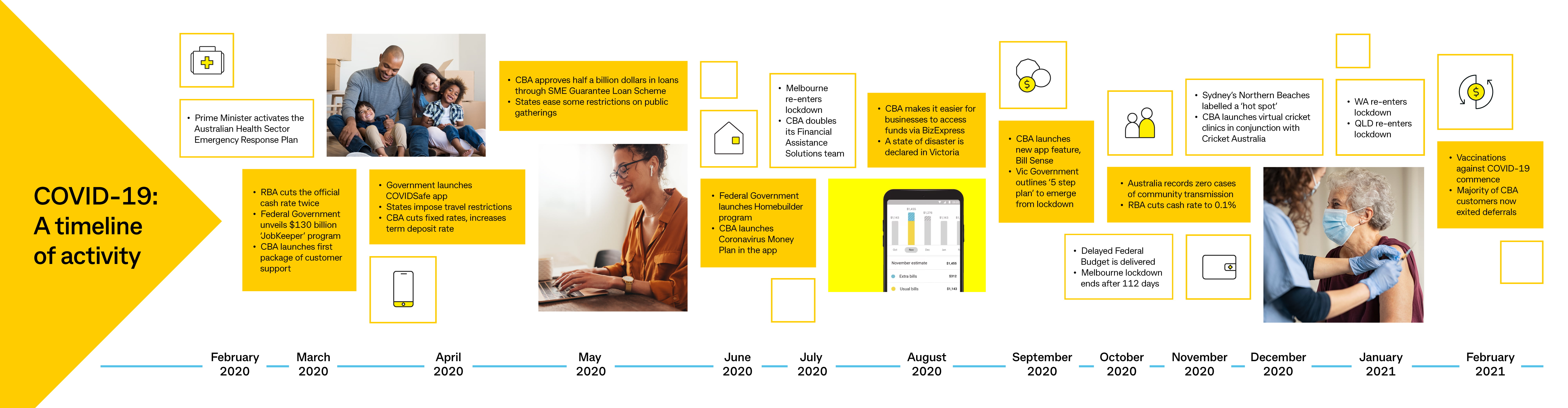

Download high-resolution infographic

JPG 1.04MBClick this infographic to view it in high-resolution.

For home loan customers, the essential measure of support was an extensive program of mortgage deferrals that started to kick in during the weeks after 10 March said Angus Sullivan, Group Executive, Retail Banking Services.

“It was really front of our mind, how we could really ‘show up’ for our customers and support them through the pandemic,” Mr Sullivan commented.

Equally important was the help provided to the bank’s some 80,000 small and medium sized business customers who were provided with automatic loan repayment deferrals, a move that was also announced on 10 March, said Mike Vacy-Lyle, Group Executive, Business Bank.

That package of support also included a waiving of a number of fees, among them merchant terminal fees, early redraw fees on business term deposit accounts, and farm management deposit accounts.

“We were able to auto-defer roughly 80,000 business loans to the value of $19 billion. The auto-deferral process took a lot of friction out of the deferral application process for small businesses,” said Mr Vacy-Lyle, who joined CBA just a month before the COVID-19 outbreak took hold in Australia.

“We were also able to, in terms of the SME government guarantee schemes, mobilise $1 billion of funding to small businesses, which represents approximately 60 cents in every dollar that has been lent to small businesses to help them through the pandemic.”

In addition to the financial support the bank provided customers, CBA’s Group Executive Institutional Banking and Markets, Andrew Hinchliff, said Commonwealth Bank also endeavoured to communicate as openly and effectively as possible with government and other organisations.

“The collaboration between government and corporates in Australia was world-leading,” he said.

“Throughout the crisis, there was real-time information flowing between all of the big organisations across the country and the government. This ensured we had the right level of fiscal and monetary support. It allowed us to come out the other side far stronger than many other countries across the globe. It just shows how powerful we can be as a country when we do get that flow between government and corporate right.”

Visit this page for a full range of support provided by CBA to customers and the country during COVID-19.