When preparing to buy an investment property it’s important to get the financial foundations right first, including working out how much you can spend, so you don’t end up over-committing to a property that puts pressure on your budget.

These five steps can help you get your foot on the investment property ladder.

Step 1: Get a deposit and work out how much you can borrow

Where are you getting the deposit for your potential investment property purchase? Do you have savings in cash, or will you use equity in your existing home?

Equity is the difference between the current value of your property and the amount you owe on your home loan. Most lenders will let you access up to 80% of your property value (this can vary between institutions).

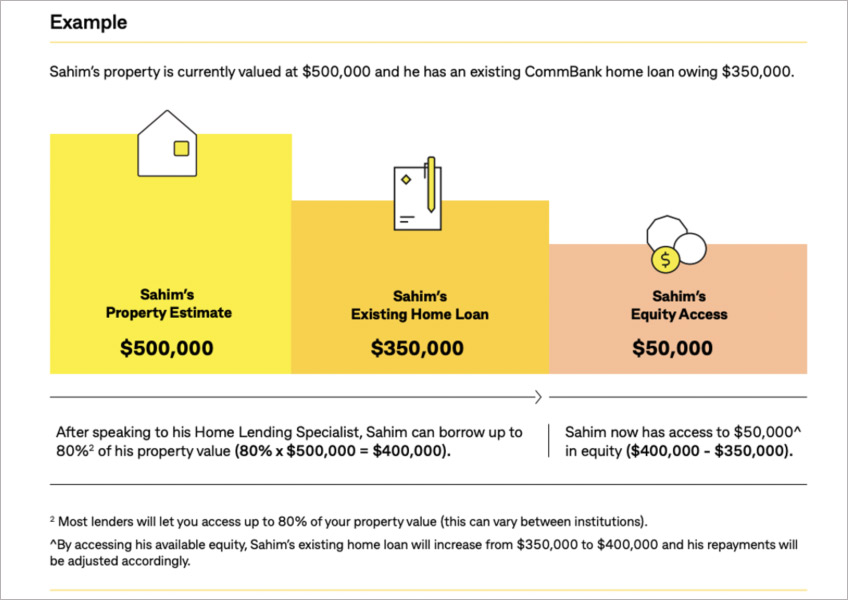

Example

Sahim’s property is currently valued at $500,000 and he has an existing CommBank home loan owing $350,000.

- Sahim’s property estimate: $500,000

- Sahim’s existing home loan: $350,000

- Sahim’s equity access: $50,000

After speaking to his Home Lending Specialist, Sahim can borrow up to 80% of his property value (80% x $500,000 = $400,000).

Sahim now has access to $50,000 in equity ($400,000-$350,000). By accessing his available equity, Sahim’s existing home loan will increase from $350,000 to $400,000 and his repayments will be adjusted accordingly.

Once you know your deposit, you can work out your borrowing power. Your deposit plus borrowing power gives you a clear idea of your property shopping budget.

In addition to the deposit, you’ll also need to budget for the other costs of owning an investment property.

Step 2: Decide your investment strategy

Next, work out what you want to achieve from your investment property. Do you want a property that generates a high income and is profitable from day one? Or are you comfortable funding a small shortfall every month, with a long-term goal of paying down the debt while the property increases in value?

These types of questions will help you work out what type of property investment and gearing strategy suits you best. This will also help you work out what type of property is more suitable: a capital growth property, or one that generates high yield.

Capital growth is the amount a property increases in value over time, while yield is the 'return' you receive on a property investment, most commonly in the form of rent. Generally, high-growth properties are often more expensive and negatively geared, and high-yield properties are more affordable and positively geared.

Step 3: Begin researching property

Now that you have an idea of what you want to get out of property investment, you can start considering the type of property you want to buy and its location.

Properties near public transport, healthcare, retail, childcare and other amenities are typically more sought after. They may cost more initially, but they generally also attract higher rents.

Once you’ve decided where you’d like to buy, look at the sale and rental prices of comparable properties in the area to get a good idea of what your rental yield is likely to be. Our Home Lending Specialists can provide you with customised Property and Suburb Reports for a comprehensive snapshot of any property or suburb you’re interested in.

Step 4: Choose the right loan

Different types of investment loans can help you achieve different results. CommBank investment home loans are available with a range of options such as fixed and variable interest rates, access to offset accounts and redraw, and interest-only payment periods.

Consider which features are important to you, so you can tailor your investment loan to suit.

Step 5: Settle and manage your investment property

Settlement day proceeds the same as it would when buying your own home, except you don’t collect the keys and move in. Instead, you engage a property manager and begin finding a new tenant, or take over the lease agreement with the existing tenant.

With an experienced property manager and relevant insurance in place, your investment property journey continues.

We're here to help

Read our complete guide to investing in property, made easy. Our expert lenders can help guide you through the entire process from start to finish. Once you’re a landlord, working with a property manager can help you manage tenants and your property going forward.