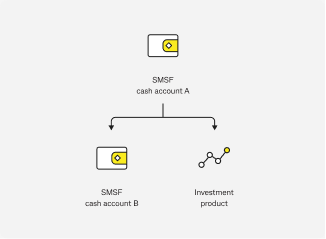

What is an SMSF cash account?

Learn how to move your super into a self-managed super fund (SMSF) and begin making contributions.

Moving your super into a Self-Managed super fund (SMSF) involves setting up an SMSF cash account and registering the fund with the ATO.

Before rolling over super from another fund, your SMSF must have an Australian Business Number, Tax File Number, bank account and Electronic Service Address (ESA) set up. You will need the ATO to confirm your fund’s status, as other funds won’t transfer money to your SMSF until they can see your fund listed on the official register of all super funds as confirmed.Once your SMSF is ready, you can add money through rollovers and contributions, and invest in line with super rules.

Once your SMSF is ready, you can add money through rollovers and contributions, and invest in line with super rules.

Rolling over super into your SMSF

What is a rollover?

A rollover is the transfer of existing super from one super fund to another, such as from an industry or retail fund into an SMSF.