Monthly Household Spending Intentions – August 2020

Each month, analysis by CBA’s Global Economic and Markets Research team provides an early indication of spending trends across seven key household sectors in Australia. In addition to home buying, the series covers around 55 per cent of Australia’s total consumer spend across; retail, travel, education, entertainment, motor vehicles, and health and fitness.

Retail Spending Intentions

- Retail spending intentions pulled-back in August, consistent with our high-frequency CBA credit/debit card spending data which clearly showed the impact of the lockdowns in greater Melbourne on household spending.

- The softness in August was most evident in reduced spending on clothing and footwear and a pull-back in general retail and the very strong household furnishings and equipment sector.

- While only accounting for a small fraction of retail spending, it is interesting to see significant strength in spending on pet shops, digital apps, electronic stores and record stores.

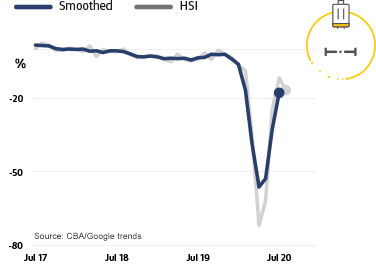

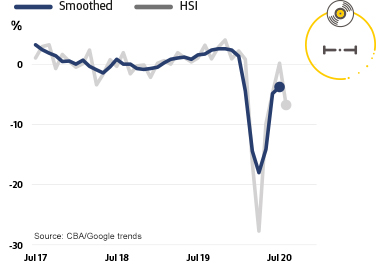

Travel Spending Intentions

- The recovery in travel spending intentions evident in recent months stalled in August, impacted by the restrictions imposed in Victoria.

- Significant weakness remains evident, not surprisingly, in spending intentions for airlines, cruise ships, travel agents, hotels, motels & resorts, bus lines and car rentals. There has been some improvement, however, in spending intentions on aquariums and campervans.

- With international borders to be closed for an extended period, a sustained improvement in travel spending intentions will be reliant on Australians holidaying within Australia and would be supported by an opening up of state borders.

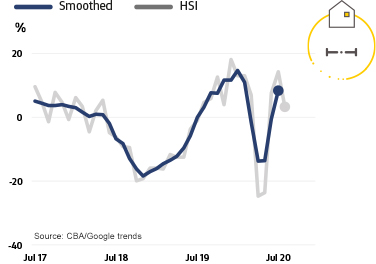

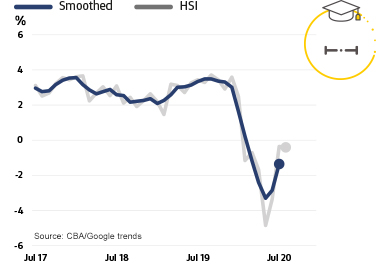

Home Buying Spending Intentions

- Home buying spending intentions for August retreated from their July highs. While there was a further increase in home loan applications, Google searches related to home buying declined slightly on the month.

- The lockdowns in greater Melbourne and the expected decline in Australia’s population growth rate will likely both weigh on home buying intentions in the months ahead.

- But the RBA’s substantial easing of monetary policy has seen mortgage rates fall to multi-generational lows and we expect these low interest rates to provide support to home buying. We have revised our house price forecasts for a peak-to-trough decline of -6% (previously -10%), but with substantial deviation expected across the capital cities.

Education Spending Intentions

- Education spending intentions were little changed in August, with some softness in spending and in Google searches for the education sector.

- While the number of transactions for spending on colleges and universities was down in August, the value of these transactions was higher. This could have been impacted by timing differences in paying tuition fees during the COVID-19 period. In addition there were modest declines in spending on school services and trade & vocational institutions.

- This softness was partially offset by increased spending on correspondence schools and elementary & secondary schools.

Entertainment Spending Intentions

- Entertainment spending intentions pulled-back a little in August, reversing some of the sharp improvement in recent months off the April low.

- Spending intentions were led lower in August by declines in food (eating out and restaurants) and alcohol spending on licensed premises.

- Weakness was also evident in August in spending on massage parlours, art galleries, live music venues, billiards venues, dance studios, movie theatres and musical theatre.

- Some strength in August was seen in spending on take-away alcohol, candy & confectionery, pay TV services, digital books and video games.

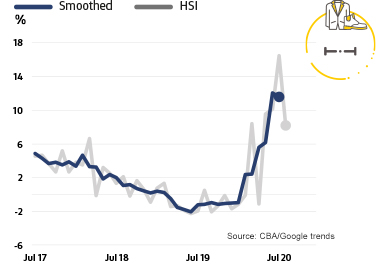

Motor Vehicles Spending Intentions

- Motor vehicle spending intentions picked up in August and are back in positive territory for the first time since the start of the COVID-19 pandemic.

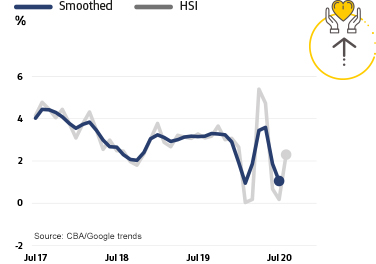

Health & Fitness Spending Intentions

- Health & fitness spending intentions picked up in August. While actual spending was a little lower on the month, Google searches related to health saw an increase.

- Areas of strength in health & fitness spending remain bicycle shops and service, golf courses and sporting goods stores.

- There was, however, a clear pull-back in August on spending for medical care, i.e. doctors, hospitals, medical laboratories and osteopaths.

Notes for Editors:

About our monthly Household Spending Intentions series

The HSI series offers a forward-looking view by analysing actual customer behaviour from CBA’s transactions data, along with household search activity from Google Trends.

The approach focuses on Australian households and their spending intentions. Employing near real-time spending readings from CBA’s household transactions data and combining them with relevant search information from Google Trends was used to map the data results on consumer spending. Households are the dominant part of the economy and drive much of its activity and volatility, and this combination adds to insights on prospective household spending trends in the Australian economy.

Google Trends is a publically available service that enables people to explore search trends around the world. These searches provide insights into what consumers are doing/researching on the Internet and what their spending intentions are.

CBA’s Household Spending Intentions series is published on the third Tuesday of every month. To find out more about the series, visit www.commbank.com.au/spendingintentions.

Disclaimer

The ‘CBA Household Spending Intentions’ series and “CBA credit and debit card spend” reports provide general market-related information, and are not intended to be an investment research report. These reports have been prepared without taking into account your objectives, financial situation (including the capacity to bear loss), knowledge, experience or needs. Before acting on the information in these reports you should consider the appropriateness and, if necessary seek appropriate professional or financial advice, including tax and legal advice. The data used in the ‘CBA Household Spending Intentions’ series is a combination of the CBA Data and Google Trends™ data. Google Trends is a trademark of Google LLC. Where ‘CBA data’ is cited, this refers to the Bank proprietary data that is sourced from the Bank’s internal systems and may include, but not be limited to, credit card transaction data, merchant facility transaction data and applications for credit. The Bank takes reasonable steps to ensure that its proprietary data used is accurate and any opinions, conclusions or recommendations are reasonably held or made as at the time of compilation of this report. As the statistics take into account only the Bank’s data, no representation or warranty is made as to the completeness of the data and it may not reflect all trends in the market. All customer data used or represented in this report is anonymous and aggregated before analysis and is used and disclosed in accordance with the Commonwealth Bank Group’s Privacy Policy Statement.

Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945.

Full disclosures and disclaimers.