Help & support

We provide loans to invest in shares or managed funds, or to release equity in existing holdings for further investments.

With roots stretching back to 1996, we understand the challenges clients and advisers face when managing an investment loan during all market cycles.

Investment loans are for:

With an investment loan, you can trade through the broker or adviser of your choice, including directly with CBA’s own online stockbroker, CommSec for self-directed customers. Self-directed clients will be provided with a CommSec Share Trading Account for a fully integrated borrowing and trading experience.

Once you or your adviser has established an investment loan, you can transfer shares, managed funds or cash as collateral. We automatically calculate the lending value based on your holdings, which determines how much you can borrow. You or your adviser can invest directly into shares and managed funds or use the funds in conjunction with other investment purposes.2

Accelerate your wealth creation: Boost your potential capital growth and income by using your Investment Loan to buy more shares or managed funds for your portfolio.

Diversification across varied companies, industries and countries, can help manage your investment risk. The extra purchasing power of our Investment Loan allows you to diversify as opportunities arise.

Realise the equity in your portfolio - harness its borrowing power with our Investment Loan. Defer capital gain (and loss) events, and build a larger portfolio at the same time.

Obtain potential tax deductions by claiming interest expenses. Bring forward interest expenses by prepaying interest. Potentially reduce your tax liability by buying more stocks that pay franked dividends.

A regular gearing plan combines the power of gearing with the discipline of regular savings, helping you build wealth over the long term.

Choose from a range of interest rate and repayment options - with no minimum loan balance requirements - to create the Investment Loan that suits you best.

If at any time you need to access the capital in your loan security, you can sell assets and transfer available funds online - effectively having cash on call when you need it.

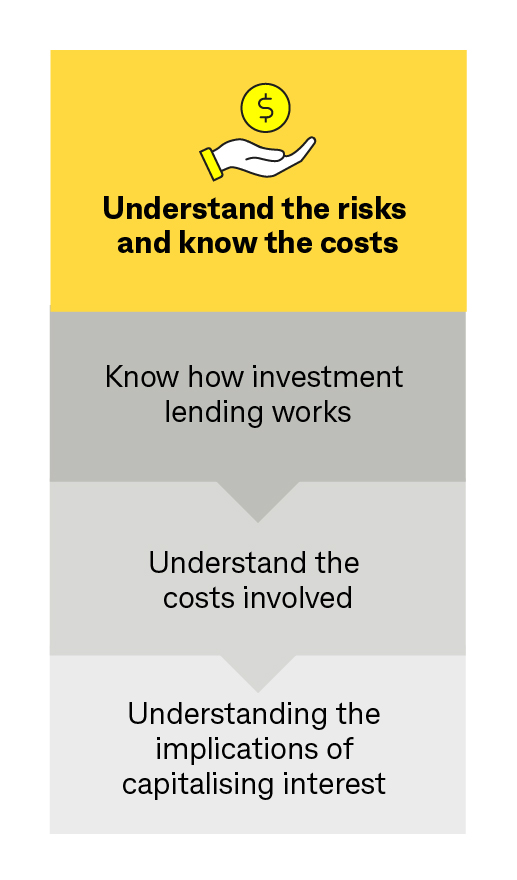

Borrowing to invest can multiply investment returns in a rising market. However, it can also multiply investment losses if the market declines and your investments perform poorly. Some of the risks of using an investment loan include:

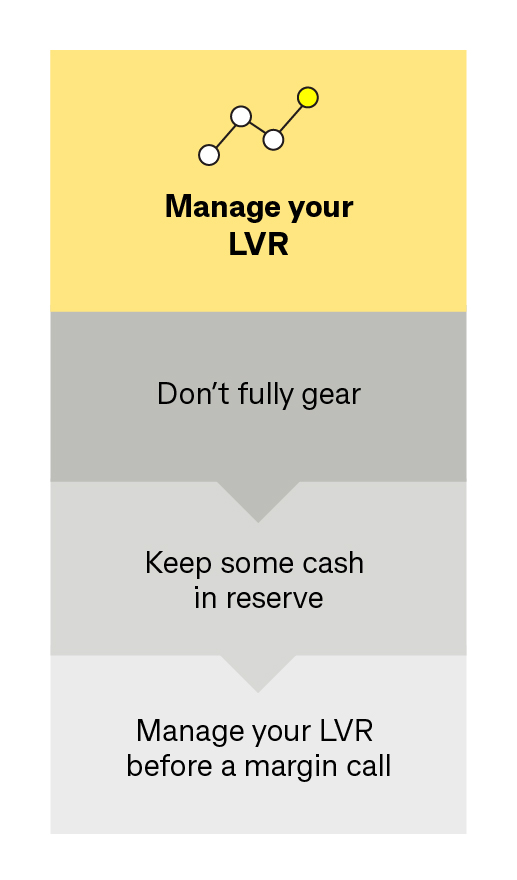

There are ways to manage the risks associated with an Investment Loan. They include:

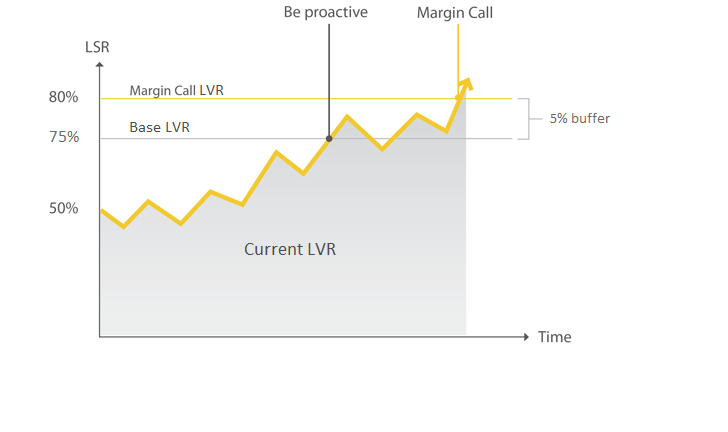

It is important to regularly monitor the status of your Investment Loan. A downturn in the market or a reduction in the borrowing limit of a listed security or fund securing your investment loan may move your Current LVR closer to your Base and Margin Call LVR.

Investors should always aim to keep their Current LVR below the Base LVR – the maximum permitted level of gearing. Once the Current LVR moves above the Base LVR, the investment loan is in the ‘Buffer’. If the Current LVR reaches and exceeds the Margin Call LVR the investor will be in Margin Call and will be required to bring the Current LVR back below the Base LVR. This is usually done by reducing the loan balance and/or adding approved securities to the portfolio.

We offer investment loans to wholesale clients who meet eligibility criteria1. With a minimum credit limit of $1 million, the Commonwealth Bank Geared Investments Loan for wholesale client offers:

As loans may not fit a standard template, investment loans can be tailored to suit clients with:

Where credit limits are above $5 million or bespoke arrangements are required, a credit assessment will be required including a financial assessment.

Wholesale Investment Loan application forms and Accepted Securities Lists can be found on our Geared Investments Form page.

This information can be found in the Geared Investments Loan Product Disclosure Statement (PDS).

Interest rates are subject to change without notice and are indicative only. Actual rate and other fixed terms and firm rates are available on application. Rates for Geared Investments Loan include trail commission (where applicable).

If you have any questions, please contact us via email, or call our team on 13 15 20.

View the tools & forms section.

Fixed vs Variable Interest Calculator

This calculator allows you to determine the potential interest savings between a fixed and variable interest rate on your loan balance over different terms.

View the FAQs section.

13 15 20, +61 2 8397 1221 (outside Australia)

Monday – Friday 8.00am – 6.00pm (Sydney time)

Locked Bag 34, Australia Square NSW 1215

Business Development Manager - New South Wales

Margin Lending

Commonwealth Bank Geared Investments Loan is issued by Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945. This product is administered by Commonwealth Securities Limited ABN 60 067 254 399 AFSL 238814 (CommSec), a wholly owned but non-guaranteed subsidiary of the Commonwealth Bank of Australia. CommSec is a Market Participant of ASX Limited and Cboe Australia Pty Limited, a Clearing Participant of ASX Clear Pty Limited and a Settlement Participant of ASX Settlement Pty Limited. Applications for Geared Investments Loans are subject to approval. Fees and charges apply. The information has been prepared without taking into account your objectives, financial situation or needs. For this reason, any individual should, before acting on this information, consider the appropriateness of the information, having regards to their objectives, financial situation or needs, and, if necessary, seek appropriate professional advice. You can view the Geared Investments Loan Product Disclosure Statement and Geared Investments Loan Terms and Conditions, and should consider them before making any decision about these products and services.

We are not authorised to carry on business in any other jurisdiction other than Australia. Accordingly, the information contained in this Internet site is directed to and available for Australian residents only.

While we have made reasonable efforts to source and display accurate and reliable information, we cannot make any representations or warranties as to the completeness and accuracy of the data displayed by our site. Readers are advised to check any important item(s) with us before making any decisions

The Commonwealth Bank is a signatory to the revised Banking Code of Practice. Read more information about the Banking Code of Practice

1 Wholesale status is qualified by either a valid Qualified Accountants Certificate OR evidence of collateral with minimum $2.5 million in value.

2 Other investment purposes only apply for non-natural applicants and excludes residential property investment purposes. Please refer to the Geared Investments Loan Terms and Conditions and Product Disclosure Statements available on our website for more information