Help & support

Your credit score is a number that indicates your creditworthiness, or ability to repay your bills on time. Generally, the number is between 0 and 1,000.

If you have a high credit score, this means you’re rated more likely to pay back a loan. This will increase your ability to borrow money, and you may also be offered a better interest rate by lenders.

Lenders such as banks, credit card companies, utilities and telcos can use your score. It helps them decide how much they'll lend you and may impact the interest rate you’re offered.

Keep in mind, however, that these lenders may have other criteria as well.

When you know your score, it can help you make smarter financial decisions.

Rest assured, when you access your credit score through a credit reporting body, it's a 'soft' enquiry (see below) – so your score won't be affected simply by checking.

A hard enquiry is when a lender checks your credit file before approving you for a loan (like a mortgage, car loan or credit card).

Checking your own credit report is called a “soft” enquiry.

Your credit score won't be affected by a soft enquiry, but it can be affected by a hard enquiry.

Knowing your credit score can be especially useful when you're looking for a loan or credit product such as:

Making a major purchase or consolidating your debts

Looking to buy a house

For ongoing expenses

Split your purchases or repayments over time

Access additional funds whenever you need

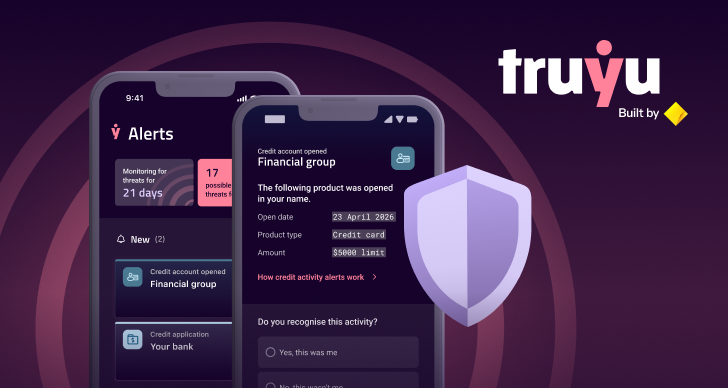

Truyu monitors identity and credit checks for you. If something unusual pops up – like a loan application in your name – you’ll know fast, so you can act faster. Get your free identity protection scan and review your credit activity today.

Generally, improving your credit score takes a little time and requires you to maintain a healthy credit history. Here are some suggestions:

Credit reporting bodies obtain information from a number of sources, and this is used to calculate your credit score.

Scores can frequently change, and some common reasons for this include:

Staying on top of your credit score can be helpful

Your credit score is a number (generally between 0 and 1,000) that indicates your creditworthiness. Your Comprehensive Credit Report includes information about:

The CCR enables credit providers to obtain a more comprehensive view of your financial situation before they choose to approve your application for credit.

The four major Australian banks, CommBank, ANZ, NAB and Westpac (plus lenders owned by them), currently supply 100% of their personal credit account information to credit reporting bodies.

Yes, information about financial hardship arrangements can appear on your credit report. A credit report can show that a financial hardship arrangement has been entered for the credit account, although it won’t include the reason for the hardship nor the details of the arrangement.

During a financial hardship arrangement, your repayment history will show whether or not you have met the requirements of the financial hardship arrangement (instead of your usual payment obligations).

Financial hardship information cannot be used by credit reporting bodies in the calculation of your credit score (except where you have failed to keep to an arrangement and this is reflected in your repayment history), and can only remain on your credit report for 12 months.

Your credit providers will first have to update the information with credit reporting bodies (you can contact them directly to check why your credit report doesn’t reflect any recent changes).

Credit scores are calculated by an algorithm that uses information from your credit report. This information includes patterns in your credit history, characteristics of your credit profile, and aspects of your credit applications.

Patterns in your credit history can include:

Characteristics of your credit profile:

Aspects of your credit applications:

Credit scores help with understanding your credit wellbeing. Your credit report and credit score are used by lenders to evaluate your creditworthiness, for example to understand your debt levels and how you manage your credit obligations. These are one of the inputs into making a credit decision, such as approving a new credit application or changing an existing credit arrangement.

Having a good credit score can come with many advantages, such as savings on interest rates or better terms on credit products.

Each of the credit reporting bodies has its own credit score algorithm. This interprets the information held in a credit report and calculates your credit score from that data.

Key reasons why your scores could differ across the credit reporting bodies include:

Information in your credit file can only be changed or removed if it's incorrect or out of date.

If there's incorrect information on your credit report summary, you should first contact the organisation that provided it.

If they don't resolve the issue, you can also contact the credit reporting body and explore their corrections process:

If there are incorrect details on your report, you should first contact the organisation that provided them.

If the organisation doesn't resolve the issue, you can also contact the credit reporting bodies and explore their corrections process.

When you apply for a credit product, the provider may record an enquiry on your credit report. This is regardless of whether your application was approved or rejected. It doesn't indicate if the product was ever taken out or remains active – nor whether it's been paid off or the account is closed.

How enquiries affect your credit score will depend on how frequent and recent they were. It will also depend on the type of credit and provider.

Credit enquiries can stay on your credit report for five years, and only be removed if incorrect or out of date.

A default is recorded on your credit report if your payment of $150 or more is overdue by 60 days or more.

Your credit provider must first send you a written notice to recover the payment, and let you know that it intends to list a default on your credit report.

If a default has been recorded and you’ve since repaid the amount in full, that payment will be noted on your credit report.

A default is kept on your credit report for five years, even after the amount has been repaid.

If you're in financial difficulty, and at risk of not making a payment, contact your credit provider as soon as possible. You can request hardship assistance.

Credit scores are calculated based on the information held on your credit file. Depending on the type of information and its status, it can be held on your file for a varying amount of time.

If you’re a victim of fraud, or are likely to be, a temporary ban can be requested on your credit report. This means your credit report and any personal information can’t be used or disclosed by a credit reporting body during the ban period. You can request a ban by contacting the major credit reporting bodies in Australia, Experian, and Equifax. A ban initially lasts for 21 days and is free to request and extend.

You can also monitor for changes in your credit report with Truyu’s Alerts subscription, which notifies you when credit applications or accounts are opened in your name. Get the app now.

If you have any questions or concerns about your credit report or credit score, you can get in touch with the credit reporting bodies directly:

Experian

Equifax

The information on this page is intended to provide general information in summary form for educational purposes. It does not have regard to the financial situation or needs of any reader and must not be relied upon as financial product advice.