Help & support

11.85% p.a. average returns delivered by Lifestage options for members aged 22–56 over the last three years up to 31 March 2026.*

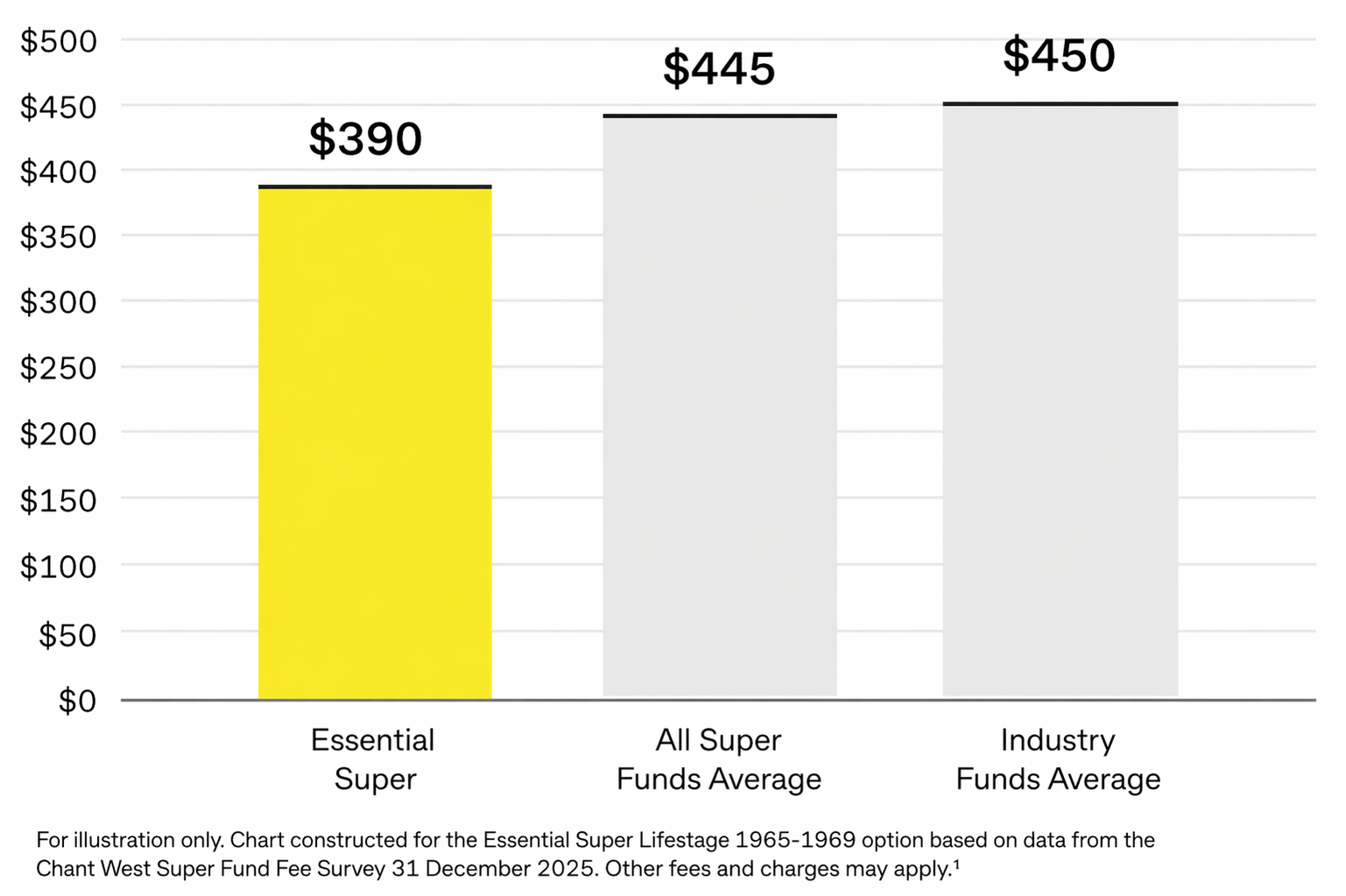

Fees lower1 than the super funds average, including industry funds.

See your super up close and alongside your everyday banking in the CommBank app – Australia’s best banking app 16 years in a row.2

See how Essential Super compares with average funds based on a $50,000 super balance.¹

Whether you prefer to set and forget or take control, Essential Super gives you flexibility with how your super is invested.

Explore your options and past performance.

When you open an Essential Super account, your money is automatically invested in a Lifestage option that’s designed to adjust your investment mix as you age.

Prefer to take control? After opening your account, you can choose from a range of other investment options.

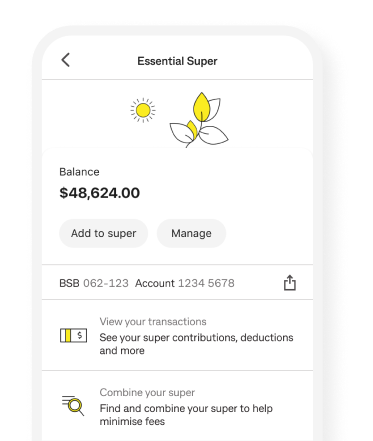

You can view your super balance, make contributions and directly click through to Colonial First State (CFS) to manage your super account, all via your CommBank app.

Insurance cover is subject to eligibility and acceptance by the insurer

Lifestage default cover will automatically be applied on the account once eligibility is met unless you opt out

You should read the full Product Disclosure Statement (PDS) and Reference Guides before making a decision

The Target Market Determination (TMD) outlines who this product is designed for and any distribution conditions.

Looking for more information about super? We’ve broken it down and made super simple in the Essential Super Learning Hub.

We’ve put together a helpful guide to help break down how superannuation in Australia works and how it can help you today - not just down the track.

Learn about the different types of investment options and what might be right for you.

Discover the key factors to consider when choosing a super fund.

You could save on fees by consolidating your super.4

Send a message in the CommBank app or call 13 22 21, 8am – 8pm (Syd/Melb time).

Give your employer a few details so your super is paid into your Essential Super account. All you need to fill out is your Essential Super account number and employer details.

Call CFS on 13 40 74, 8:30am - 6pm (Syd/Melb time), Mon-Fri or +61 2 9197 3000 from overseas. Email CFS at [email protected].

In NetBank or the CommBank app, you can:

View your super balance

Make a personal contribution

Click through to CFS to manage and make changes to your super

Here are some important documents and forms that include information about funding and managing your account.

Fund name: Essential Super ABN: 56 601 925 435 USI / SPIN: FSF1332AU

Yes, here are ways you can save on super tax.

We’ve teamed up with Colonial First State (CFS) to bring you Essential Super.

CFS is the provider of Essential Super and one of Australia’s largest superannuation providers. CFS has helped over 3 million Australians with their super, investment, and retirement savings since 1988, giving you confidence that your super is in expert hands.

Use CFS' tools and calculators to find out how much super you need and what your super will look like in retirement.

You can access super when you retire after reaching your preservation age, when you turn 65, or in special circumstances such as a temporary resident permanently leaving Australia.

About withdrawing super

Departing Australia Superannuation Payment

If you’ve changed jobs or super funds, it’s possible some of your super has been left behind.

There are usually only two places it could be:

With one of your previous super funds

Held by the Australian Taxation Office (ATO), waiting for you to claim it

Thankfully, tracking lost super is not difficult.

1 The fee comparison is for MySuper products. This fee comparison is based on the Lifestage 1965-69 investment option for a member balance of $50,000 and may vary for different age cohorts. The Chant West Super Fund Fee Survey compares the Lifestage option that is closest to 71% growth assets, which is consistent with the average risk and return profile of most non-lifecycle products. Total fees and costs include administration fees and costs, investment fees and costs and net transaction costs on a gross of tax basis. Fund averages are calculated by Chant West on a weighted average basis.This comparison has been prepared by CFS using data sourced from the Chant West Super Fund Fee Survey, effective 31 December 2025 and is based on information provided to Chant West by third parties, that is believed accurate at the time of publication. Fees may change in the future which may affect the outcome of the comparison. Chant West may make adjustments to fees and costs for comparison purposes and therefore data may vary to other published materials. Whilst care has been taken to ensure that the data provided by Chant West is correct, CFS neither warrants, represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Additional fees may apply. Refer to the PDS and Fees and Investments Reference Guide to find out more.

2 Awarded ‘Bank of the Year – Digital Banking’ for 2025 (for the 16th year in a row) by Canstar in May 2025.

3 Please see the PDS and Insurance Reference Guide for specific terms that apply to insurance cover in Essential Super, including what’s not covered. For at least the first two years of your Lifestage cover, you generally won’t be paid a benefit if it is due to a pre-existing condition (Limited cover). Generally, a pre-existing condition is an illness or injury that you were aware of at any time before your cover commenced or increase. This exclusion will no longer apply if you're capable of working for 30 consecutive days either immediately before the two year period ends or at any time after the two year period ends. Additional exclusions also apply.

Any information provided by CBA may include general financial product advice but does not consider your individual objectives, financial situation, needs or tax circumstances, and so you should consider the appropriateness of the advice having regard to your circumstances before acting on it. You should read the PDS and the Reference Guides for Essential Super carefully and consider whether the information is appropriate for you before making any decision regarding this product.

4 The information provided does not take your personal objectives, financial or taxation situation or other needs into account. If you need advice on your personal circumstances, please talk to a financial adviser. Before you make a decision to consolidate your super, you should compare the costs, fees, risks and benefits of your other super funds against Essential Super. It makes sense to consider whether you can replace any insurance cover you may lose upon rolling over, potential costs for withdrawing from other super funds, as well as any investment or tax implications.

* Past performance is not a reliable indicator of future performance.

The 3‑year return is calculated on a cumulative year‑on‑year basis and annualised up to 31 March 2026, averaged across the Lifestage options for those born between 1970 and 2004. The return is an average across 7 Lifestage options where the majority of Essential Super members are invested.

Lifestage returns shown below are cumulative year-on-year basis and annualised on a 3-year period up to 31 March 2026:

1970-74: 10.86%

1975-79: 11.63%

1980-84: 11.98%

1985-89: 12.11%

1990-94: 12.09%

1995-99: 12.09%

2000-04: 12.16%

Returns are calculated after fees (excluding the dollar-based administration fee) and 15% tax on earnings and are calculated by the change in unit price for the relevant option during the period. Individual returns may vary. See the latest returns for all Lifestage options. Returns and calculations are provided by CFS.

^ Essential Super was recognised for 'Exceptional Super for Gen Z’ and ‘Low Fee Super – High Growth' in Mozo Experts Choice Awards 2025. For more information, visit Mozo.

Essential Super was awarded 'Best-Value Super Fund for Young People' as part of the 2026 Money Magazine Best of the Best awards. For more information, visit Money Magazine.

Avanteos Investments Limited ABN 20 096 259 979, AFSL 245531 (referred to as Colonial First State, CFS, ‘we’, ‘us’ or ‘our’) is the Trustee of Essential Super ABN 56 601 925 435 and the issuer of interests in Essential Super. Essential Super is distributed by the Commonwealth Bank of Australia ABN 48 123 123 124, AFSL 234945 (the Bank). The CFS Group consists of Superannuation and Investments HoldCo Pty Limited ABN 64 644 660 882 (HoldCo) and its subsidiaries, which includes CFS. The Bank holds an interest in the CFS Group through its significant minority interest in HoldCo.

This information is issued by CFS and may include general financial product advice but does not consider your individual objectives, financial situation, needs or tax circumstances, and so you should consider the appropriateness of the advice having regard to your circumstances before acting on it. The Target Market Determination (TMD) for Essential Super can be found at cfs.com.au/tmd and includes a description of who the financial product is appropriate for and any conditions on how the product can be distributed to customers. You should read the Product Disclosure Statement (PDS) and the Reference Guides for Essential Super carefully and consider whether the information is appropriate for you before making any decision regarding this product. Download the PDS and Reference Guides at commbank.com.au/essentialsuper-documents or call us on 13 4074 for a copy.

None of the Bank, HoldCo, CFS, nor any of their respective subsidiaries guarantee the performance of Essential Super or the repayment of capital by Essential Super. An investment in this product is subject to risk, loss of income and capital invested. An investment in Essential Super is via a superannuation trust and is therefore not an investment in, deposit with or other liability of the Bank or its subsidiaries.

The insurance provider is AIA Australia Limited ABN 79 004 837 861, AFSL 230043 (AIA Australia). AIA Australia is not part of the Commonwealth Bank Group or CFS. Insurance cover is provided to eligible members of Essential Super under policies issued to CFS.

Please refer to the Group Privacy Statement and the CFS Privacy Policy for more information about how your personal information is collected, used and shared.

The CommBank app is free to download however your mobile network provider charges you for accessing data on your phone. You should refer to your mobile phone plan or contact your provider to find out more. Terms and conditions are available on the CommBank app. NetBank access with NetCode SMS required. Find out about the minimum operating requirements on the CommBank app page. The CommBank app is available on Android operating systems 8.0+ and iOS operating system 15.0+.