Help & support

Unlike a home, buying the right investment property is a financial decision. So, it’s important to understand the goals and strategies behind a successful property investment.

Step-by-step guide to buying an investment property?

Having a clear plan is your first step towards buying an investment property.

Find the right investment property

Understanding why you want to own an investment property will help you choose the right one to buy and decide what rent to charge.

Explore step-by-step guide for investing in property

Get the essentials with property estimates and suburb insights to help you search, shortlist and decide. Research a property, understand the neighbourhood and take the next step when you’re ready to buy.

Buying a property may take time, but investing doesn’t have to.

With the CommBank app*, you can explore investing options through shares, ETFs and managed funds – helping your money work harder between property investment purchases and your next investment goal.

The Federal Budget 2026/27 made recommendations to change the landscape around negative gearing. Before making any decisions around investing in property, ensure you first speak with a tax agent and source up-to-date advice that takes your personal circumstances into account.

Read more about the proposed changes to negative gearing.

Once you have saved for your deposit, calculated your borrowing power with our easy-to-use calculator, chosen your investment strategy and researched property options, you can apply online or with one of our Home Lending Specialists.

Buying an investment property is a decision predominately based on financial considerations, unlike purchasing a home to live in. Property investors have strategies in mind behind purchasing that can impact the type of property to buy as well as goals that they want to achieve.

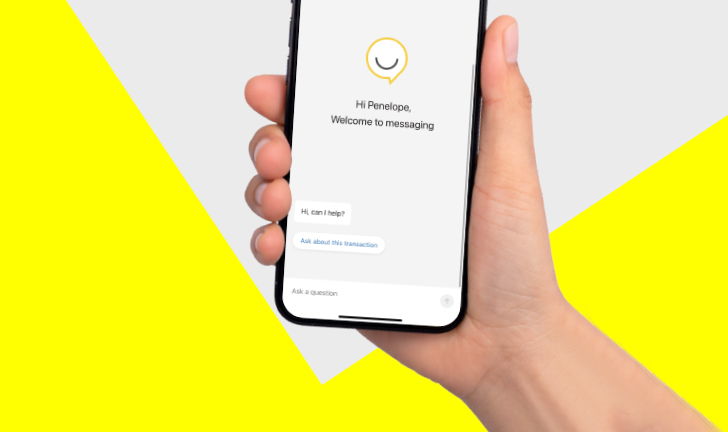

Get help from Ceba in the CommBank app or connect with a specialist who can message you back. You’ll need CommBank app notifications turned on so you know when you’ve received a reply.

Book instantly to speak to a Home Loan Specialist at a time that suits you.

Redraw, change your repayments or loan type to better meet your needs and more.

Fast-track your call, see expected wait times and connect with a specialist in the CommBank app.

Get instant help from our virtual assistant or chat to a specialist.

Subject to credit approval. Fees, charges, terms and conditions apply. As this advice has been prepared without considering your objectives, financial situation or needs, you should consider its appropriateness to your circumstances before acting on the advice.

*The CommBank app is free to download however your mobile network provider charges you for accessing data on your phone. You should refer to your mobile phone plan or contact your provider to find out more. Terms and conditions are available on the CommBank app. NetBank access with NetCode SMS required. Find out about the minimum operating requirements on the CommBank app page.