Help & support

A home loan Australians choose. 1 in 5 customers chooses CommBank for their home loan.20

Get into your first home sooner. Over 5x low-deposit options designed to help first home buyers enter the market faster.21

Expert help, wherever you are. Get guidance from one of over 1,400 Home Lending Specialists across Australia.22

Helping more first home buyers succeed. Supporting more than 80,000 first home buyers into home ownership.23

Conditional pre-approval provides an estimate of how much you could borrow based on the information you provide to us. It is confirmation from us that you’re eligible to apply for a home loan up to a certain limit and helps you understand what you can afford without any obligation to take up the loan. This shows sellers you are serious about buying and that you are confident you can afford the property when making an offer.

When providing conditional pre-approval, CommBank will consider your personal financial situation and the property price range you’re looking at. If something changes – your financial situation, for example – you can always update your conditional pre-approval.

When you speak to a lender it is good to have an idea of the property price range you’re interested in, how much deposit you have saved, your income and current living expenses and any changes to your circumstance in the foreseeable future.

Conditional pre-approval is valid for: 90 days.

You can apply anytime online, or make an appointment with help from one of our Home Lending Specialists. They’ll let you know exactly what documents you’ll need for your application.

Estimated time to complete home loan application: 10 minutes when you apply online.

Before signing the Contract of Sale, you need to negotiate your offer and conditions on the purchase of the property. Home-in provide step-by-step expert guidance and digital convenience to support you with these conversations so that when you (buyer) and the vendor (seller) are ready to sign the contract, you are comfortable with the selling price, settlement terms and any other conditions for the sale.

Some things to do and look out for before signing the Contract of Sale:

After signing the Contract of Sale this needs to be submitted to CommBank to complete any necessary and final checks (e.g. property valuation, credit checks, building documents). After this you will be provided formal approval within 1-5 business days and sent your loan offer documents to review and sign. Your Home Lending Specialist is there to help walk you through the documents and any questions you might have. Other steps to consider:

Settlement is when the purchase of the property is completed, and it officially becomes yours. We will arrange a settlement date, time and location with your solicitor or conveyancer and notify you by SMS as soon as settlement is completed. What you need to do:

Estimated time from application to settlement: 4-6 weeks.

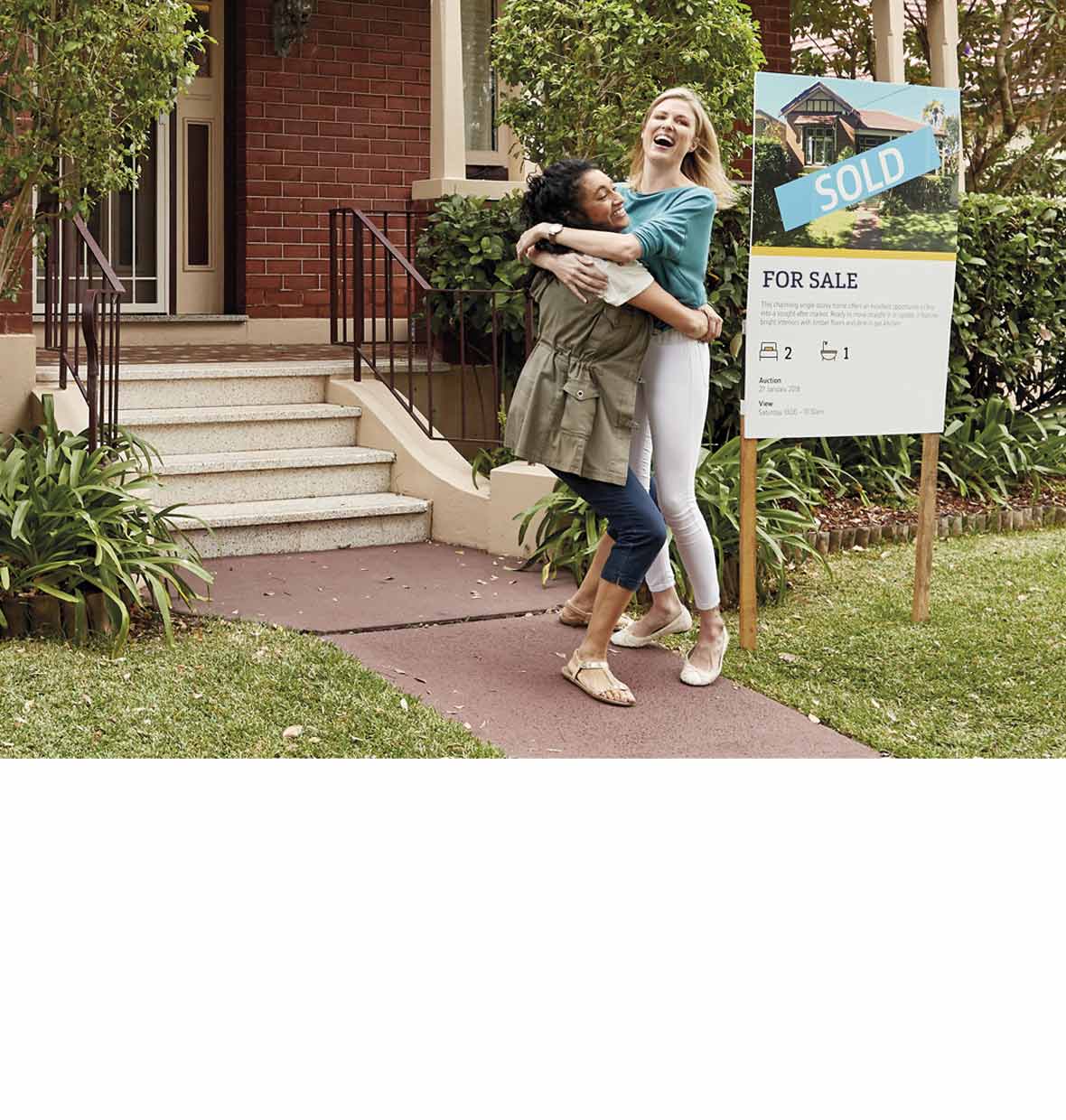

Congratulations! You’ve bought the property.

You can start your home buying journey in the CommBank app – Buy a home. Access to guidance, tools and insights, from saving for your home loan through to the home buying process.

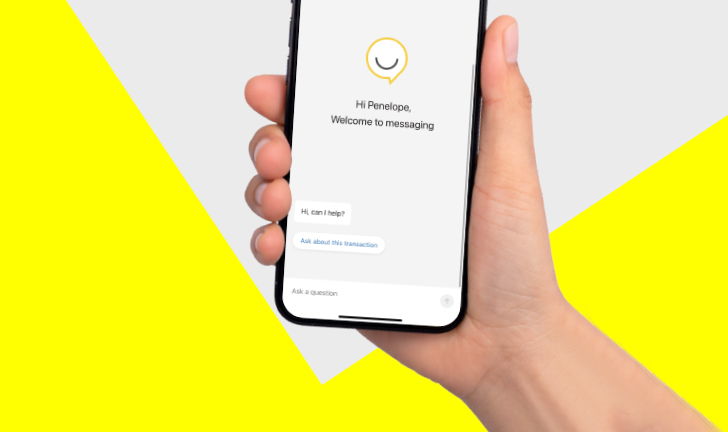

Get help from Ceba in the CommBank app or connect with a specialist who can message you back. You’ll need CommBank app notifications turned on so you know when you’ve received a reply.

Book instantly to speak to a Home Loan Specialist at a time that suits you.

Redraw, change your repayments or loan type to better meet your needs and more.

Fast-track your call, see expected wait times and connect with a specialist in the CommBank app.

Get instant help from our virtual assistant or chat to a specialist.

This advice has been prepared without taking your individual objectives, financial situation or needs into account. Before acting on this advice, you should consider whether it is appropriate to your circumstances. Applications for finance are subject to approval. Full terms and conditions will be included in the Bank’s loan offer. Home Insurance is provided and issued by Hollard Insurance Partners Limited ABN 96 067 524 216, AFSL 235030 (Hollard) and distributed by the Commonwealth Bank of Australia ABN 48 123 123 124, AFSL 234945 (CBA). Hollard is not part of the CBA Group. CBA and its related entities do not sell, issue or guarantee the obligations or performance of Hollard or the products Hollard offers and this insurance product does not represent a deposit with or liability of either CBA or any of its related bodies corporate. If you purchase a Home Insurance policy, CBA is paid a commission which is a percentage of your premium.

For products issued by Hollard, information about the target market can be found within the product’s Target Market Determination available here.

A Product Disclosure Statement (PDS) is available at all Commonwealth Bank branches, by downloading them from commbank.com.au or by calling 13 2423 and should be considered before making any decisions about this product. You should also read the Premium, Excess and Discount Guide (PEDG), Key Facts Sheers (KFS) and Financial Services Guide (FSG) by clicking on the links, or by calling 13 2423 for a paper copy.

Our staff may receive payments for business they refer to other persons in the Bank who specialise in certain products and/ or services and may be eligible for prizes including overseas travel and gift vouchers. Our staff may also receive benefits such as tickets to sporting and cultural events, corporate promotional merchandise or other similar benefits from product providers whose products they may sell or for business they may refer to product providers. We may receive commission for the sale of Home Insurance provided by Hollard. The commission amount ranges from 0% to 15% of the premium paid (excluding government charges). . Commonwealth Bank of Australia ABN 48 123 123 124 AFSL and Australian credit licence 234945. Registered office: Ground Floor, Tower 1, 201 Sussex Street, Sydney, NSW 2000.

20 Figure based on CommBank’s 20.54% Australian Prudential Regulation Authority (APRA) market share as of June 2026 (includes Unloan; excludes RMG).

21 Includes Australian Government 5% Deposit Scheme, Australian Government Help to Buy Scheme, Lenders Mortgage Insurance (LMI), Low Deposit Premium (LDP), and Guarantor Support.

22 Data reflects CommBank branch, mobile and direct Home Lending Specialists in Australia as of 30/06/2026. Excludes Premier Banking, Business Home Lending and Private Banking specialists.

23 Data represents home ownership through Australian Government 5% Deposit Scheme backbook as at 30/06/2026.