Help & support

Found the perfect new home? A Bridging Loan covers the time between buying a new property and settling on the sale of your existing one.

CommBank bridging loans have a maximum loan term of 12 months.

A Bridging Loan allows you to purchase a new home before finalising the sale of your existing one.

Avoid having to rent somewhere because you’ve sold your current home before finding a new one.

Within the term of your loan.

Save on interest while having access to your money by using an Everyday Offset account.*

Bridging loans have a maximum loan term of 12 months – so you need to sell and settle your current property within this timeframe.

A Bridging Loan is not available on all home loans, and you may incur some fees and charges depending on your loan type.

A Bridging Loan is generally an Interest Only loan for the 12-month period. The longer it takes you to sell your current home, the longer you’ll be charged interest on the bridging loans.

If you don’t sell your home in the agreed period, we may get involved to sell the property. We may also charge you a default interest rate above the annual percentage rate applying at the time or adjust the interest rate by removing any discretionary margin in place. You may be better off asking for an extended settlement period or selling your existing home first.

For more information, you can refer to our guide on Bridging Loans.

Make an appointment with one of our Home Lending Specialists to discuss whether a Bridging Loan may be right for you and your circumstances.

A bridging loan is a short-term loan that helps you buy a new property before you've sold your existing one. It covers the financial gap between the purchase of your new home and the sale of your current property. CommBank can offer eligible applicants bridging loans with a maximum term of 12 months, allowing you to avoid the hassle of renting or aligning settlement dates perfectly.

A bridging loan lets you purchase a new property before selling your current one by providing short-term financing. During the bridging period, which can last up to 12 months, you typically only pay interest on the loan. Once your existing property is sold, the proceeds are used to repay the bridging loan.

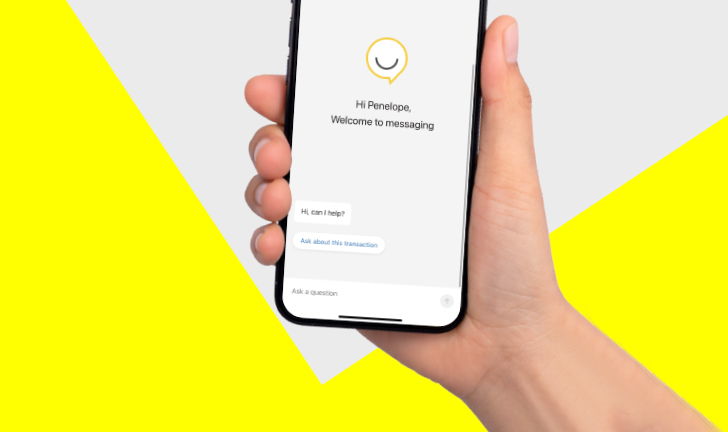

Get help from Ceba in the CommBank app or connect with a specialist who can message you back. You’ll need CommBank app notifications turned on so you know when you’ve received a reply.

Book instantly to speak to a Home Loan Specialist at a time that suits you.

Redraw, change your repayments or loan type to better meet your needs and more.

Fast-track your call, see expected wait times and connect with a specialist in the CommBank app.

Get instant help from our virtual assistant or chat to a specialist.

* An Everyday Offset is a transaction account linked to your eligible variable rate home loan or investment home loan. Money you put into your Everyday Offset reduces the balance on which we charge interest. No interest is earned on the balance of your Everyday Offset account, even if it exceeds the balance of the eligible home loan.

The target market for these products will be found within the product’s Target Market Determination, available here.