Help & support

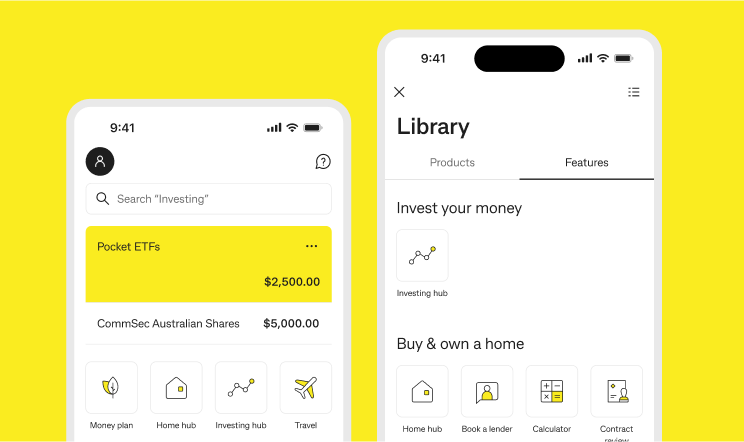

Always wanted to invest, but not sure where to start?

Log in to the CommBank app and tap the ‘Investing hub’ tile from your app dashboard or Library to start exploring.

Everyday Investing

Invest in up to four professionally designed funds with as little as $2 per investment1

Designed for

People who want to invest in diversified funds and have their investments managed by professionals

Investor experience

Beginner

Minimum investment

$2 per investment

Pocket ETFs

Begin with as little as $50 and choose from ten themed ETFs

Designed for

People who have just started investing or want to invest in specific industries like tech

Investor experience

Beginner to moderate

Minimum investment

$50

CommSec Aussie Shares

Invest in over 2,000 Australian shares that are listed on the Australian Stock Exchange (ASX)

Designed for

People who enjoy the freedom and control that comes with choosing their own investments

Investor experience

Moderate to advanced

Minimum investment

$500 for your first trade in any investment, then $100 in the same investment after that

Provided by Colonial First State

Choose how your money is invested and track your balance in NetBank or the CommBank app.

Already an Essential Super member? Go to the Essential Super Hub

Whether you’re looking to invest in shares, ETFs or cash options, SMSF solutions offer flexibility and control to suit your goals.

Provided by AIA Financial Wellbeing

A qualified financial planner provides tailored advice to help you define your investment strategies, plan for your future and achieve your wealth goals.

With AIA Financial Wellbeing, get advice for financial decisions big or small and only pay for the advice you receive – there’s no long-term commitment.

Savings accounts and Term Deposits

Choose the right account for your savings goals.

Access your cash when you need it with our range of flexible savings accounts or lock it away and earn a fixed return with our Term Deposit options.

Thinking about investing in property?

We have the knowledge and tools you’ll need to help you find your ideal investment, build your portfolio and choose the right loan.

Was the information on this page useful?

1 Colonial First State Investments Limited (CFS) ABN 98 002 348 352, AFSL 232468 is the responsible entity of the managed funds and issuer of the financial products offered under Everyday Investing. The Everyday Investing suite of financial products are distributed by the Commonwealth Bank of Australia ABN 48 123 123 124, AFSL 234945 (CommBank). Commonwealth Private Limited (CPL) ABN 30 125 238 039, AFSL 314018, a wholly-owned non-guaranteed subsidiary of CommBank has been appointed as the Investment Manager by CFS for the managed funds. The CFS Group consists of Superannuation and Investments HoldCo Pty Limited ABN 64 644 660 882 (HoldCo) and its subsidiaries, which includes CFS. CommBank holds an interest in the CFS Group through its significant minority interest in HoldCo.

This information may include general advice but does not take into account your individual objectives, financial situation, needs or tax circumstances, and so you should consider the appropriateness of the advice having regard to your circumstances before acting on it.

The Target Market Determination (TMD) for the financial products can be found on Everyday Investing Important Documents and includes a description of who the product is appropriate for and any conditions on how the product can be distributed to customers. You should read the Terms and Conditions (T&Cs), Product Disclosure Statement (PDS) and Financial Services Guides (FSGs) carefully before making a decision about acquiring or continuing to hold these products and consider talking to a financial adviser before making an investment decision. You can get the T&Cs, PDS and FSGs on Everyday Investing Important Documents or by calling 13 22 21.

Neither CommBank, CFS Group, nor any of their respective subsidiaries guarantee the performance of the financial products or the repayment of capital. An investment in any of the financial products is subject to risk, loss of income and capital invested. Everyday Investing is not an investment in, deposit with or other liability of CommBank or its subsidiaries. This information is based on current requirements and laws as at the date of publication.

2 The fee comparison is for MySuper products. This fee comparison is based on the Lifestage 1965-69 investment option for a member balance of $50,000 and may vary for different age cohorts. The Chant West Super Fund Fee Survey compares the Lifestage option that is closest to 71% growth assets, which is consistent with the average risk and return profile of most non-lifecycle products. Total fees and costs include administration fees and costs, investment fees and costs and net transaction costs on a gross of tax basis. Fund averages are calculated by Chant West on a weighted average basis. This comparison has been prepared by CFS using data sourced from the Chant West Super Fund Fee Survey, effective 31 March 2025 and is based on information provided to Chant West by third parties, that is believed accurate at the time of publication. Fees may change in the future which may affect the outcome of the comparison. Chant West may make adjustments to fees and costs for comparison purposes and therefore data may vary to other published materials. Whilst care has been taken to ensure that the data provided by Chant West is correct, CFS neither warrants, represents nor guarantees the contents of the information, nor does it accept any responsibility for errors, inaccuracies, omissions or any inconsistencies herein. Additional fees may apply. Refer to the PDS and Fees and Investments Reference Guide to find out more.

Commonwealth Securities Limited ABN 60 067 254 399 AFSL 238814 (CommSec) is a wholly owned but non-guaranteed subsidiary of the Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945. CommSec is a Market Participant of ASX Limited and Cboe Australia Pty Limited, a Clearing Participant of ASX Clear Pty Limited and a Settlement Participant of ASX Settlement Pty Limited. The Commonwealth Direct Investment Account is issued by Commonwealth Bank of Australia ABN 48 123 123 124 AFSL 234945. This product is administered by Commonwealth Securities Limited. The target market for this product can be found within the product’s Target Market Determination, available at commbank.com.au/tmd.

The information has been prepared without taking into account your objectives, financial situation or needs. For this reason, any individual should, before acting on this information, consider the appropriateness of the information, having regards to their objectives, tax and financial situation or needs, and, if necessary, seek appropriate professional advice.

You can view the CommSec Notice Investor Terms and Conditions, CommSec Share Trading Terms and Conditions (PDF), Best Execution Statement, International Shares Terms and Conditions, CommBank Transaction Savings and Investment Account Terms and Conditions and our Financial Services Guide (PDF) and should consider them before making any decision about these products and services.

Investing in overseas markets exposes you to risks including those related to movements in foreign currency exchange rates and market prices.

^Essential Super was recognised in Mozo Experts Choice Awards 2025. For more information, visit Mozo.

The information has been prepared without taking into account your objectives, financial situation or needs. For this reason, any individual should, before acting on this information, consider the appropriateness of the information, having regards to their objectives, financial situation or needs, and, if necessary, seek appropriate professional advice.

You can view the CommSec Share Trading Terms and Conditions (PDF), CommBank Transaction Savings and Investment Account Terms and Conditions, Best Execution Statement, CommSec Pocket Terms and Conditions and our Financial Services Guide (PDF) and should consider them before making any decision about these products and services.

To operate a CommSec Pocket account, you’ll need an eligible CommBank transaction account. Please consider the full terms and conditions which are available on request. CommSec Pocket is free to download however your mobile network provider may charge you for accessing data on your phone. Investing carries risks. The value of your investment may go down as well as up. The minimum allowable size of your investment is subject to fluctuations in ETF unit prices. Brokerage is charged at $2 per trade, for trades up to $1,000 and 0.20% for trades above $1,000. Consider the PDS for each ETF prior to making an investment decision. Past performance is not an indicator of future performance.

Avanteos Investments Limited ABN 20 096 259 979, AFSL 245531 (referred to as Colonial First State, CFS, ‘we’, ‘us’ or ‘our’) is the Trustee of Essential Super ABN 56 601 925 435 and the issuer of interests in Essential Super. Essential Super is distributed by the Commonwealth Bank of Australia ABN 48 123 123 124, AFSL 234945 (the Bank). The CFS Group consists of Superannuation and Investments HoldCo Pty Limited ABN 64 644 660 882 (HoldCo) and its subsidiaries, which includes CFS. The Bank holds an interest in the CFS Group through its significant minority interest in HoldCo.

This information is issued by CFS and may include general financial product advice but does not consider your individual objectives, financial situation, needs or tax circumstances, and so you should consider the appropriateness of the advice having regard to your circumstances before acting on it. The Target Market Determination (TMD) for Essential Super can be found at cfs.com.au/tmd and includes a description of who the financial product is appropriate for and any conditions on how the product can be distributed to customers. You should read the Product Disclosure Statement (PDS) and the Reference Guides for Essential Super carefully and consider whether the information is appropriate for you before making any decision regarding this product. Download the PDS and Reference Guides at commbank.com.au/essentialsuper-documents or call us on 13 4074 for a copy. If you need advice on your personal circumstances, please talk to a financial adviser.

None of the Bank, HoldCo, CFS, nor any of their respective subsidiaries guarantee the performance of Essential Super or the repayment of capital by Essential Super. An investment in this product is subject to risk, loss of income and capital invested. An investment in Essential Super is via a superannuation trust and is therefore not an investment in, deposit with or other liability of the Bank or its subsidiaries.

The insurance provider is AIA Australia Limited ABN 79 004 837 861, AFSL 230043 (AIA Australia). AIA Australia is not part of the Commonwealth Bank Group or CFS. Insurance cover is provided to eligible members of Essential Super under policies issued to CFS.

AIA Financial Wellbeing is operated by AIA Financial Services Pty Limited ABN 68 008 540 252 AFSL 231109 (AIA Financial Services), a subsidiary of AIA Australia Limited ABN 79 004 837 861 AFSL 230043 (AIA Australia). Commonwealth Bank has a referral arrangement with AIA Financial Wellbeing to provide advice to Commonwealth Bank customers on life insurance and simple wealth needs across a range of financial solutions from different providers. AIA Financial Wellbeing, AIA Financial Services and AIA Australia are not part of the Commonwealth Bank Group and Commonwealth Bank does not guarantee and is not responsible for the financial advice provided by AIA Financial Wellbeing, the performance of products recommended by AIA Financial Wellbeing or the obligations of AIA Financial Wellbeing, AIA Financial Services and AIA Australia.