Help & support

A home loan repayment typically consists of two parts:

With an Interest Only home loan, your minimum repayments will only cover the interest charges on your loan for an agreed period of time.

This means your loan balance won’t reduce during the interest-only period, since you are not making any principal repayments.

Interest rates for Interest Only home loans tend to be higher than Principal & Interest home loans (where your payments cover both the principal and the interest).

An interest-only period is available for CommBank Investment home loans and Owner Occupied home loans.

Because you’re only paying the interest amount off your loan during your Interest Only period, you’re not paying the loan balance (principal component), which means you’ll pay more interest over the life of your loan.

If you pay both the Principal and Interest you’ll reduce your loan balance earlier in the loan term, which means the amount of interest payable will also reduce, because interest is calculated on the outstanding balance of your home loan.

You can switch between Principal and Interest repayment and Interest Only payment options during the life of your loan. However, there are limits for how long you can have Interest Only periods.

These limits apply when you request a new or extended Interest Only payment.

When your Interest Only period expires, your home loan repayments will change to Principal and Interest. This means your repayments will increase as you start paying off your loan balance.

To prepare for this change and remain in control of your repayments, make sure you know your expiry date and plan accordingly. You can also find out more about your Interest Only maturity.

To find the expiry date for your CommBank home loan, log on to NetBank > View account > Account Information. Make sure you select your Interest Only home loan from the drop-down list.

With an Interest Only loan you choose to make payments that only cover the interest amount (for a set period). Interest Only payments are lower than if you were paying both the Principal and Interest components, however your loan balance isn’t reducing.

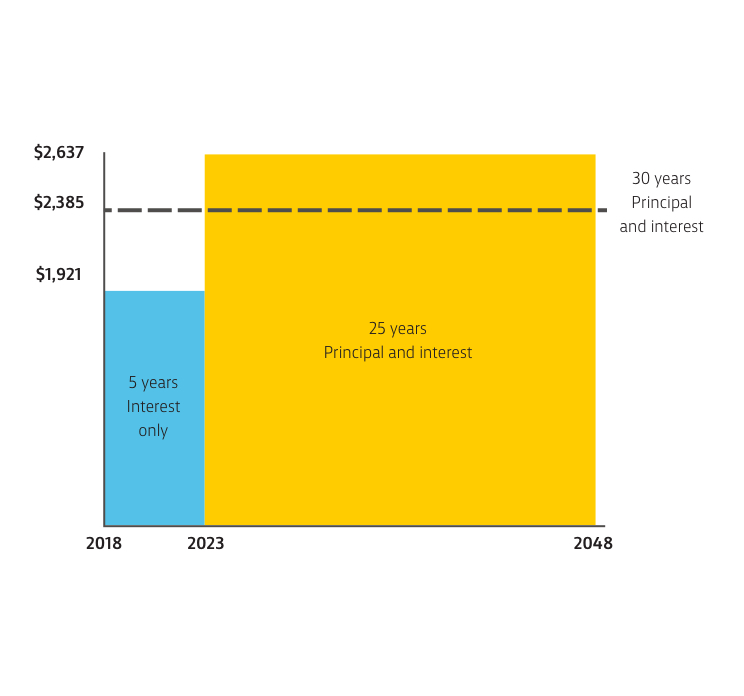

At the end of an Interest Only period, the balance of the loan must be paid back to the bank over the period remaining before the end of the loan. This means that the Principal and Interest repayments will be higher than they would have been prior to the Interest Only period.

In this example, Jo has taken out a home loan of $500,000 for 30 years.1

Work out what your repayments might be using the repayment calculator.

Speak to a Home Lending Specialist about your options.

Call us on 1300 057 072 8am – 6pm Monday to Friday for your existing home loans.

If you'd like to apply for a new Interest Only home loan, book an appointment.

Explore features, rates and fees of our wide range of flexible home loans.

See at a glance our fixed and variable interest rates for CommBank home loans, whether you’re an Owner Occupier or Investor and are paying Principal and Interest or Interest Only.

Get help from Ceba in the CommBank app or connect with a specialist who can message you back. You’ll need CommBank app notifications turned on so you know when you’ve received a reply.

Book instantly to speak to a Home Loan Specialist at a time that suits you.

Redraw, change your repayments or loan type to better meet your needs and more.

Fast-track your call, see expected wait times and connect with a specialist in the CommBank app.

Get instant help from our virtual assistant or chat to a specialist.

1 Calculations are estimates provided as a guide only. They assume interest rates don’t change over the life of the loan and are calculated on the rate that applies for the initial period of the loan. Interest rates referenced are current rates and may change at any time. Fees and charges are payable. The calculations do not take into account fees, charges or other amounts that may be charged to your loan (such as establishment or monthly service fees or stamp duty).

2 Everyday Offset is a feature of our Complete Access Transaction Account which is linked to an eligible home loan, and accountholder/s must also be accountholders of the linked home loan. Interest is not charged on that part of the Home Loan balance equal to the balance of the Complete Access account.

Applications are subject to credit approval. Full terms and conditions will be included in our loan offer. Fees and charges are payable. Interest rates are subject to change.

As this advice has been prepared without considering your objectives, financial situation or needs, you should consider its appropriateness to your circumstances before acting on this advice.