Help & support

Awarded 'Bank of the Year - First Home Buyers' by Canstar for 2025*

A one-off insurance premium that can help you buy your property with a smaller deposit.

Lenders Mortgage Insurance (LMI) is a one-off, non-refundable, non-transferrable premium that's added to your home loan. It's calculated based on the size of your deposit and how much you borrow. The more you contribute to the purchase price of your property, the lower the cost will be. LMI protects the bank against any loss we may incur if you are unable to repay your loan.

The circumstances of your home loan will determine whether LMI or a Low Deposit Premium (LDP) may apply. This includes when you restructure your home loan, top it up or refinance. This is because there may be an increased risk associated with each application.

We require you to take out LMI where there is an increased risk associated with your loan.

Example

Our Home Lending Specialists can help explain when Lenders Mortgage Insurance may apply to your home loan, how much it will cost and what happens if there is a shortfall debt.

Similar to Lenders Mortgage Insurance, this additional cost can help you get your home loan with a smaller deposit.

Split the cost of a home with family or friends, while keeping individual control of your finances. Available for most home loans.

A family member can help you secure a home loan by mortgaging their own property as additional security.

You may be able to buy your first home sooner with a smaller deposit.

LMI stands for Lenders Mortgage Insurance. It’s a type of insurance that helps protect the lender in case you’re unable to repay your home loan. LMI is usually required if your Loan-to-Value Ratio (LVR) is above 80%, meaning you have a deposit of less than 20% of the property’s value. While LMI helps protect the lender, it’s important to note that the cost is typically passed on to the borrower as a one-time premium, which is added to the loan amount.

The cost of Lenders Mortgage Insurance (LMI) varies depending on several factors, including your Loan-to-Value Ratio (LVR), the size of your loan, and the lender's specific policies. Generally, LMI can range from 1% to 5% of your loan amount. For example, on a $500,000 loan with a 10% deposit, LMI could cost over $10,000. If you have a deposit of 20% or more, you typically won't need to pay LMI.

Our Home Lending Specialists can help explain when Lenders Mortgage Insurance may apply to your home loan, how much it will cost and what happens if there is a shortfall debt.

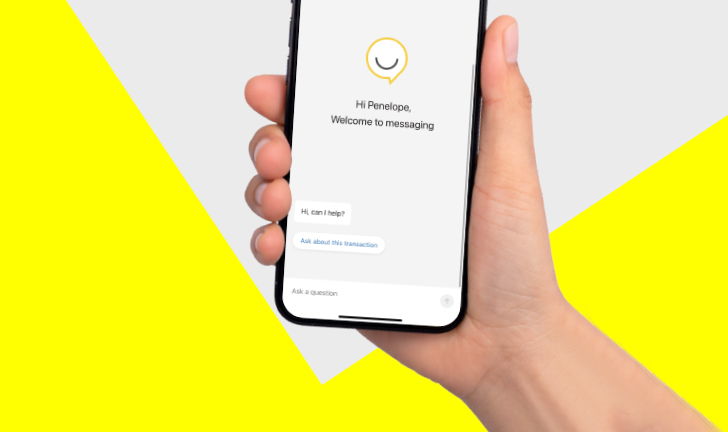

Get help from Ceba in the CommBank app or connect with a specialist who can message you back. You’ll need CommBank app notifications turned on so you know when you’ve received a reply.

Was the information on this page useful?

*Awarded 'Bank of the Year - First Home Buyers' by Canstar in July 2025.

Book instantly to speak to a Home Loan Specialist about a new loan at a time that suits you.

Redraw, change your repayments or loan type to better meet your needs and more.

Fast-track your call, see expected wait times and connect with a specialist in the CommBank app.

Get instant help from our virtual assistant or chat to a specialist.