Help & support

*Standard Variable Rate (Owner Occupied Principal and Interest) for new borrowings with Package benefits and Loan to Value ratio of 60% or below (with discount margin offer).

Simple verification. Streamlined proof of income process so you can secure your property sooner

CommBank Yello. Get access to exclusive benefits, cashbacks and discounts

Dedicated support. One of our Home Lending Specialists will guide you every step of the way

Ask for a personalised rate. Find out if you're eligible for interest rate reductions and waivers

Conditional pre-approval for 90 days. Make an offer or bid for a property with confidence

Flexible repayment options. Choose weekly, fortnightly or monthly repayments

We offer a simplified verification process for business owners with less documents to prove your income.

Get in touch with a Home Lending Specialist to discuss your options.

In some instances, we may need more information. We’ll let you know if this is the case.

Don't have these documents? Here are other options.

Digi Home Loan

A digital home loan with a low variable rate and access to one Everyday Offset account. Only available online.

Standard Variable Rate

A competitive variable rate home loan with discounts tailored to you, plus access to offset and an extensive range of features.

Simple Home Loan

A simple home loan with a competitive variable rate and the choice to access two offset accounts.

Home loan calculators

Let us do the maths for you. Calculate what your home loan repayments could be, estimate how much you could borrow, refinance and more.

Home loan tips for small business owners

There are a few things a small business owner can do to make the home loan application process as smooth as possible.

Refinancing your home loan as a business owner

Check out these six steps to help you successfully refinance your home loan.

If you don't have six months of salary credits, you may use one of the following:

If you don't have financial records showing profit and loss for the last two years, you'll need a letter from your accountant (on their company letterhead) confirming your business has:

If you’re self-employed and not eligible for simple income verification, you'll need to provide extra documentation. This may include:

This list is a general guide. Talk to a Home Lending Specialist to find out what documents you’ll need.

Examples of self-employed borrowers include:

If you earn your income through any of these structures, you're considered self-employed for the purpose of a home loan.

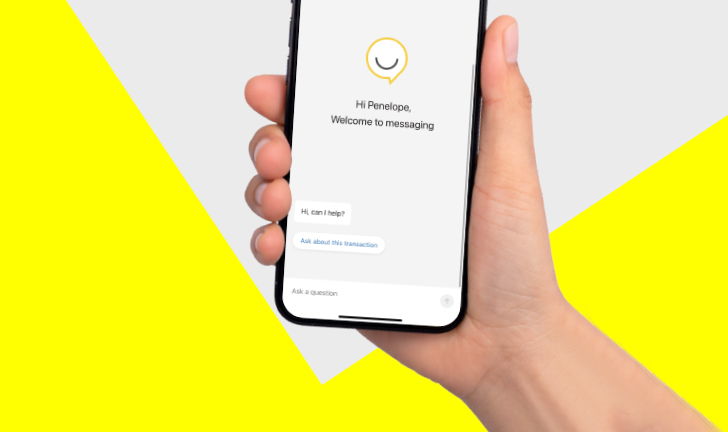

Get instant help from Ceba in the CommBank app or connect with a specialist who can message you back. You’ll need CommBank app notifications turned on so you know when you’ve received a reply.

Book instantly to speak to a Home Loan Specialist at a time that suits you.

Redraw, change your repayments or loan type to better meet your needs and more.

Fast-track your call, see expected wait times and connect with a specialist in the CommBank app.

Get instant help from our virtual assistant or chat to a specialist.

1 Wealth Package benefits apply to eligible home loans or line of credits, including any new Standard Variable Rate and Fixed Rate home loans originated on and from 14 March 2026. A non-refundable annual fee of $395 is payable in advance. The package can be established in the name of one or two individual’s name/s, or in the name of a corporate entity. It cannot be established in the name of a business or family investment trust. Please refer to the applicable product guide and Consumer Mortgage Lending Products Terms and Conditions for full details.

• This information is current as at 11 October 2024 and is for general information purposes only. It has been prepared without considering your objectives, financial situation or needs. You should consider the appropriateness of this information to your circumstances before acting on it.

The contents of this page are intended to provide general information of an educational nature only, without regard to the financial situation or needs of any reader and must not be relied upon as financial product advice. As the information has been provided without considering your objectives, financial situation or needs, you should, before acting on the information, consider its appropriateness to your circumstances. You should consider the Terms and Conditions and/or Product Disclosure Statement, as well as the Target Market Determination, of any product before deciding whether a product is appropriate for you. You should also consider seeking independent professional legal, tax and financial advice.

* Comparison rate calculated on a $150,000 secured loan over a 25 year term. WARNING: Comparison rate is true only for the examples given and may not include all fees and charges. Different terms, fees or other loan amounts might result in a different comparison rate. Comparison rates for variable Interest Only loans are based on an initial 5-year Interest Only period. Comparison rates for fixed Interest Only loans are based on an initial Interest Only period equal in length to the fixed period. During an Interest Only period, your Interest Only payments will not reduce your loan balance. This may mean you pay more interest over the life of the loan.

Calculations are not a loan approval. Applications are subject to credit approval, satisfactory security and minimum deposit requirements. Conditions apply to all loan options. Full terms and conditions will be set out in our loan offer, if an offer is made. Fees and charges are payable. Interest rates are subject to change. You should also read our Financial Services Guide.

^^$0 establishment fee offer is available on Simple Home Loan applications submitted between 6 December 2025 and 30 June 2026 inclusive through CommBank’s proprietary and broker channels. Applications submitted outside this period and via other channels are not eligible for this offer.

This offer is only available to CommBank customers who meet the following criteria:

(a) All borrowers must be individuals. Applications from trusts or companies are not eligible; and

(b) Application must be submitted through CommBank’s proprietary or broker channels, it is not available to customers that submit an application through Bankwest or Unloan.

(c) The loan must be for one of the following eligible products:

- Simple Home Loan

- Simple Investment Home Loan.

If your application does not meet the eligibility criteria, the standard establishment fees: $300 for non-off-the-plan purchases and $800 for off-the-plan purchases, will apply.

• CommBank reserves the right to withdraw or amend this offer at any time without notice.

+ To be eligible for this offer, a loan must meet the following criteria (Eligible Home Loan):

If the above conditions are met, Qantas Points will be awarded as follows:

The Qantas Points will be credited to the nominated member’s Qantas Frequent Flyer account within 30 days of settlement and will appear on the nominated member’s Points Activity Statement as ‘CommBank Digi Home Loan’. Qantas Points will not be awarded if the loan is in arrears or default, or any of the borrowers are receiving financial hardship relief or assistance at the time of crediting the points.

You should consider whether the Qantas Points will result in any tax implications for you. We suggest you seek independent advice from your accountant or tax adviser if you are uncertain of the tax implications to you.

This offer cannot be used in conjunction with any other advertised or promotional offer. We reserve the right to close or vary this offer at any time.

Home loans issued by Commonwealth Bank of Australia ABN 48 123 123 124 AFSL and Australian credit licence 234945. Commonwealth Bank of Australia pays Qantas for Qantas Points issued in relation to this offer.